The Steel Safeguard Quota Cliff-Edge Nobody Is Pricing For

Why the gap between a duty refund and a duty bill is the real risk in UK steel trade measures, and what it means for cashflow, margins and contracts.

Photo by Nithina Palanisamy

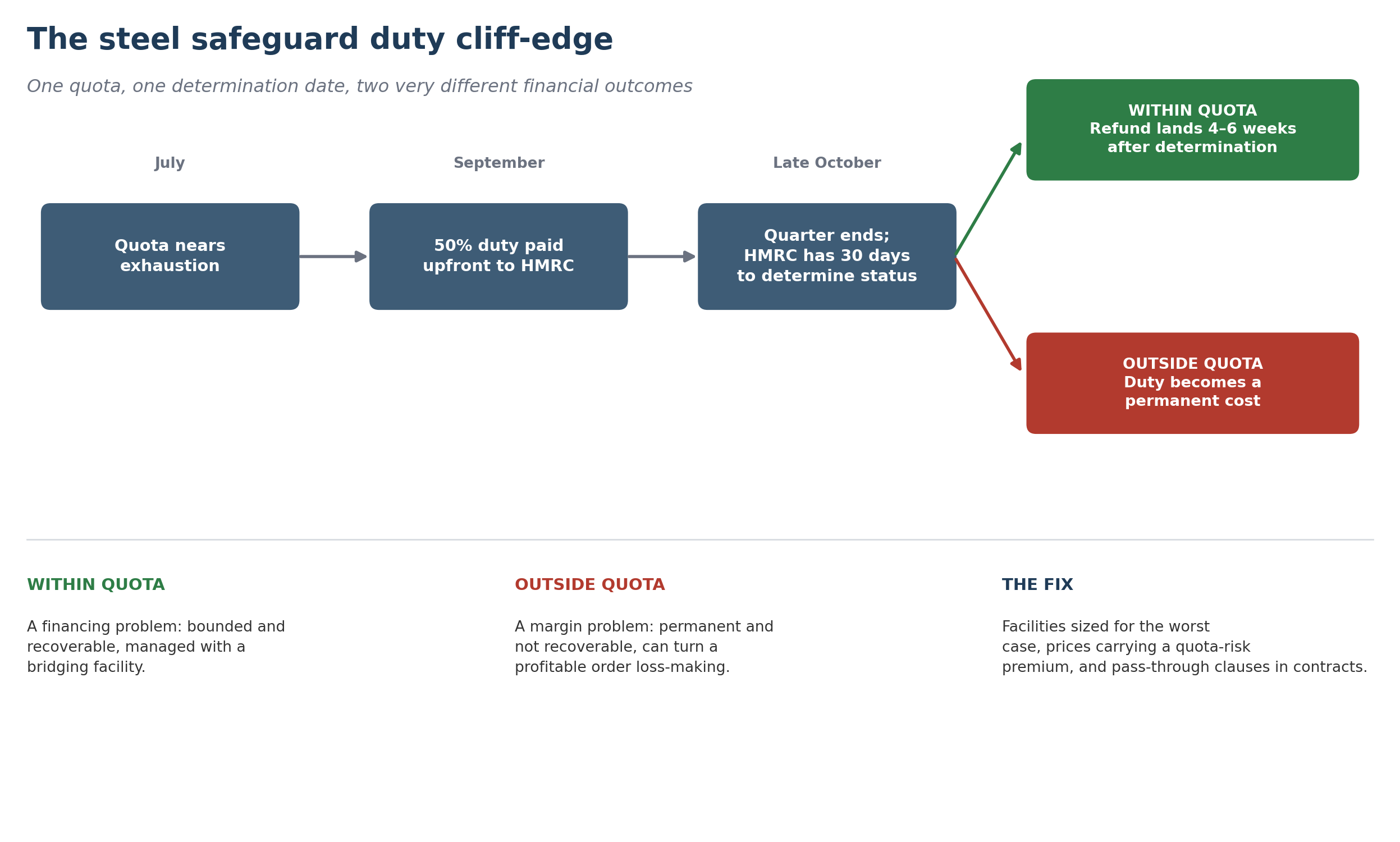

Christopher Morris (UKF Group) described on LinkedIn how steel import duty is actually paid and it deserves wider attention than it will probably get. He set out, in clear detail, the mechanics of what happens once a quota's free allowance runs out: fifty per cent duty paid up front to HMRC, a wait until the end of the quarter, a further thirty days for HMRC to determine whether the goods were within quota, and then, if you are fortunate, four to six weeks for the refund to land. An order placed in July might not see its money back until December.

The replies to that post are worth reading in full, particularly the points made on working capital impact and on consignment stock models used elsewhere to manage exactly this kind of cashflow strain. But there is a second, unasked second question to the one everyone is discussing, and it changes the shape of the problem entirely: what happens if the goods turn out to be outside quota?

Two different risks, not one

The within-quota case, the one Christopher Morris describes, is a financing problem. It is expensive and it is disruptive, but it is bounded and it is recoverable. The fifty per cent paid in July is a deposit, not a cost. It can be managed like any other financing gap: an overdraft facility, invoice discounting against the expected HMRC refund, or a dedicated duty-bridging line sized to cover four to six months of exposure. The cost is the interest on that bridge, which is unwelcome but calculable.

The outside-quota case is not a financing problem. If HMRC determines that a shipment falls outside the quota, the fifty per cent stops being a deposit and becomes a permanent cost of goods sold. At that point no amount of working capital financing helps, because there is nothing to bridge to. You are simply financing a loss rather than a delay. Given how thin margins typically run in steel distribution, a duty charge of that size on unhedged stock does not just erode margin, it can turn a profitable order into a loss-making one.

These two outcomes need to be modelled separately, not blended into a single average expectation. A business that plans on the basis that most of its stock will probably clear within quota is planning for the best case. A business that provisions for the worst case, duty not recovered, and treats any refund as upside, is the one that survives a bad quarter.

The part that makes this genuinely hard to plan for

Quota is pooled across every importer bringing in a given product category. No individual business controls when its category tips past the ninety per cent threshold that triggers the fifty per cent duty. A company can order in line with its own historic volumes, following its usual buying discipline exactly, and still be pushed outside quota by other importers' late-quarter buying that it has no visibility of and no influence over.

That is what turns this from a nuisance into a structural risk. It is close to unpredictable at the level of an individual firm, even though the aggregate drawdown across a category is perfectly knowable in principle. The practical consequence is that working capital facilities need to be sized against the whole exposed book, not against any single shipment, because any shipment in that book could be the one that lands outside quota.

A simple illustration makes the scale of this clear. Take an SME distributor importing £2 million of stainless steel a quarter, roughly £8 million a year, spread across ten shipments of £200,000 each. If they assumed, reasonably enough, that only the final shipment or two of the quarter carried real risk of landing outside quota, they might budget a facility of around £100,000, fifty per cent duty on that last shipment. But because the trigger depends on category-wide drawdown, not on where in the quarter a shipment falls, any of those ten shipments could turn out to be the one that pushes the category over the threshold. Prudent sizing therefore means providing for fifty per cent duty on the entire quarter's import value, a facility of around £1 million rather than £100,000, a tenfold difference between what instinct suggests and what the mechanism actually requires.

That £1 million is a quarterly figure, not an annual one, but it still needs careful handling on the timeline. The cash lag runs to four or five months, longer than the three-month quarter that generates it, so the following quarter's imports start accruing duty before the previous quarter's claims have been refunded. The facility therefore needs to revolve rather than reset each quarter, and the true peak a business needs to be able to fund sits somewhat above the £1 million from any single quarter, not below it, and certainly not at the flat annual total that simply multiplying by four would suggest.

Cashflow, margins and contracts

On cashflow: the base case forecast should reflect the probability of recovery, informed by how close each product category typically runs to its quota ceiling, not an assumption that duty is never recovered. What does need to be sized conservatively is the facility itself, which should carry enough headroom to cover the worst case if quota is exhausted, held as contingency rather than treated as the working assumption for pricing or day-to-day forecasting.

On margins: a fixed-margin pricing model no longer reflects reality once quota exhaustion becomes routine rather than exceptional, and current steel demand patterns suggest several categories are already running close to their ceilings for large parts of the quarter. The answer is not a willingness to accept a loss-making order if the duty lands, but a risk-loaded quoted price: the probability-weighted cost of duty, based on how close a category is running to exhaustion, built into the price charged upfront, in effect a self-insurance premium. On shipments that clear within quota this looks like a slightly better than normal margin, since the premium was not needed. On shipments that fall outside quota, the premium absorbs the duty rather than the order turning into an outright loss. If a category's odds of exhaustion rise to the point where a properly risk-loaded price becomes uncompetitive, that is the signal to reprice, pass the risk to the customer through contract, or decline the order, not to trade at a loss and hope.

On contracts: this is where the change needs to happen fastest, because contracts written on the old assumption, that duty is either zero or a known fixed rate, no longer reflect how the mechanism actually works. Purchase and sales contracts need a quota-status pass-through clause, comparable in structure to a currency or commodity pass-through, indexed to published HMRC quota utilisation data rather than to a market price. It is also worth separating, within that clause, who bears the financing cost of the four-to-six-month lag from who bears the duty itself if it is not ultimately refunded. These are different risks, and they do not naturally sit with the same party.

Why this matters

This is a real-world illustration of a wider problem with how trade remedies and carbon border mechanisms are currently being applied to UK manufacturing. The financial risk here falls on compliant UK distributors and importers regardless of whether their own trading behaviour has anything to do with the dumping or circumvention the safeguard exists to prevent. A better-designed regime would give importers real-time, category-level visibility of quota consumption, so this risk could be priced and contracted for in advance rather than discovered after the goods have already been ordered.

None of this is an argument for scrapping trade defence measures. It is an argument for designing them properly, with the operational and financial consequences considered as part of the policy, not left for industry to absorb after the fact. Anyone with a view on how this should work in practice, particularly from the distribution and procurement side, I would be glad to hear it.

Steven Raikes

Founder, Experius Consulting Ltd

Fractional CFO to UK manufacturing and engineering businesses