The Funding Mistake that Almost Broke a Good Business - How the wrong finance choice puts good companies under strain

Imagine Sarah, founder of a growing manufacturing company turning over £5 million.

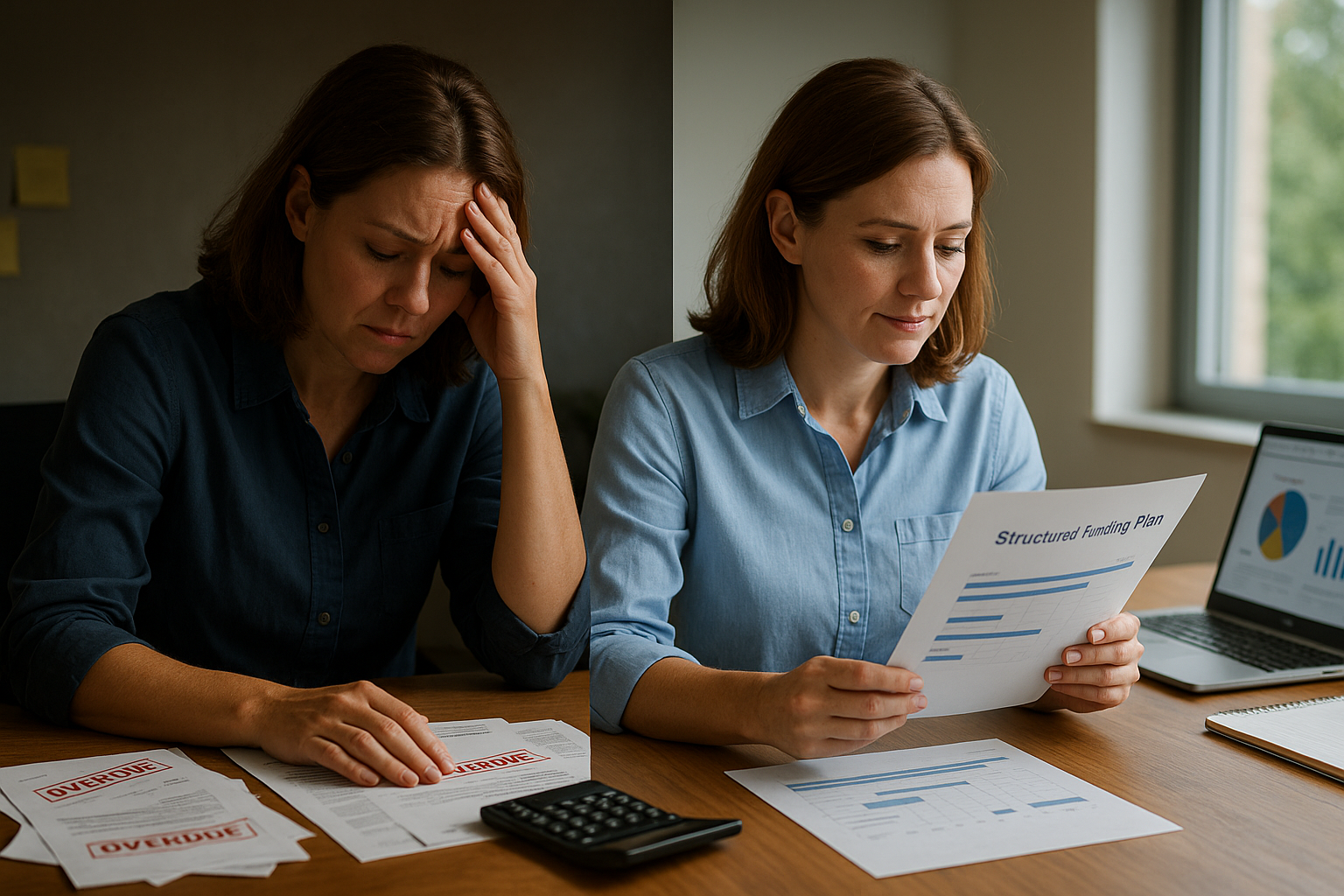

Orders were rising, but cash was tight. A major customer insisted on 90-day terms, suppliers wanted paying in 30 days, and a new machine was needed to keep up with demand. Feeling the pressure, Sarah took the fastest offer she could find: a short-term, high-cost lender who could advance funds in 24 hours.

For a few months, it felt like a lifeline. The machine was installed, wages were paid and the lights stayed on. Then the repayment schedule started to bite. Daily repayments drained cash. The effective interest rate was eye-watering. There was no room left for mistakes or delays. A couple of late payments from customers and suddenly Sarah was juggling payroll, tax and supplier demands.

The problem was not that she raised funding. The problem was that she used the wrong funding for the job.

Instead of a sustainable mix of longer-term debt for the machine and flexible working capital for the debtor gap, she used an expensive short-term product to solve a long-term need. It nearly cost her the business.

This is what Experius Consulting helps founders avoid.

Why SMEs need funding in the first place

Needing funding is not a sign of weakness. It is a normal part of running and growing a business. The key is to be clear what problem you are trying to solve.

1. Short-term working capital

This is the day-to-day cash you need to run the business.

Examples include:

Paying suppliers before your customers pay you

Funding stock or work in progress

Covering VAT or PAYE timings

Seasonal swings, such as a busy Christmas followed by a quiet January

Short-term funding is usually about smoothing the timing difference between money out and money in.

2. Longer-term working capital

Some businesses permanently need more working capital as they grow. For example:

You win larger contracts that have longer payment terms

You move into export markets where payments take longer

Your stockholding doubles because of a new product range

Here, the business has stepped up a level. The funding solution often needs to step up too.

3. Capital expenditure (capex) projects

These are bigger investments in assets that will last for years, such as:

New machinery or vehicles

Shop fit-outs or refurbishments

IT systems and infrastructure

The benefit of these assets is long term, so the funding should be long term as well.

4. Cash flow gaps and “crunch points”

These are specific points where cash is under pressure, for example:

A one-off tax bill

A contract where you start work long before you can invoice

A delay in a major customer payment

These gaps can often be planned for and funded sensibly, but if ignored they lead to panic decisions and poor funding choices.

5. Growth, acquisitions and step-changes

Finally, there are the positive reasons:

Opening a new site or region

Launching a new product line

Acquiring a competitor or complementary business

These moves can create real value if they are funded in a structured way that the business can sustain.

The main funding types in plain language

There is no single “right” answer. The right mix depends on your business model, stage of growth, appetite for risk and personal goals. Most solutions are a blend of the following.

1. Equity

Equity means selling a share of your business to investors.

Common sources include:

Friends and family

Angel investors (wealthy individuals backing businesses at an early stage)

Venture capital funds (VCs)

Crowdfunding platforms

You do not repay equity like a loan. Instead, investors receive a share of future profits and, ideally, a slice of the value when you eventually sell or refinance.

Pros

· No monthly repayments

· Can provide larger amounts of capital

Investors may bring expertise and contacts

Cons

· Dilution: you own less of your business

· You may need board seats for investors

Expectations on growth and exit can be demanding

Equity is usually most appropriate for high-growth businesses or step-change investments that cannot realistically be serviced by debt.

2. Debt

Debt is money you borrow and repay with interest.

Main forms include:

· Bank loans: fixed term, regular repayments.

· Overdrafts: flexible facility linked to your current account.

· Asset finance: funding for specific assets, such as hire purchase or leasing.

Asset-based lending and invoice finance: lending secured on stock, debtors or other assets.

Pros

· You keep full ownership of the business

· Costs can be predictable and planned

Good for funding assets and stable, recurring cash flows

Cons

· Regular repayments regardless of how trading is going

· Lenders may require security or personal guarantees

Covenants: rules you must comply with, such as debt service cover ratios

Used properly, debt is a powerful tool. Used poorly, it becomes a straitjacket.

3. Short-term and high-cost options

These are products designed for speed and flexibility, but they come at a price.

Examples include:

· Online “payday-style” business lenders

· Merchant cash advances (repayments taken as a percentage of daily card takings)

Revenue-based finance (repayments linked to turnover)

Pros

· Fast decisions and minimal paperwork

Useful as a genuine short-term bridge

Cons

· Very high effective interest rates

· Can quickly erode margins if used for ongoing needs

Daily or weekly repayments can strangle cash flow

These products are not inherently bad. The problem arises when they are used as a permanent funding solution rather than a short-term tool.

Matching the funding to the need

A simple way to think about funding is this: match the life of what you are funding to the life of the funding itself.

Key rules of thumb

1. Long-term assets = long-term funding

If you buy a machine that will last 5 years, a 5-year asset finance agreement is usually more appropriate than a 6-month working capital loan.

2. Short-term needs = short-term funding

If you are smoothing debtor days or handling seasonal stock, an overdraft or invoice finance facility is often better than long-term term debt.

3. Do not fund permanent needs with temporary money

If you are constantly using short-term, high-cost products to plug the same gap, the real problem is undercapitalisation. You either need more equity or a properly structured working capital facility.

4. Stress-test repayments against realistic trading

Always ask, “What happens if sales are 20 per cent lower than forecast, or if a big customer pays late?” If the funding only works in a perfect world, it is the wrong structure.

When mixing funding types makes sense

Most well-funded SMEs use a blend.

Example 1: New machine and working capital

A manufacturing firm wants to buy a £250k machine and knows that stock and debtor levels will rise as output increases.

A sensible structure might be:

· Asset finance or term loan over 5 years for the machine

· Increased overdraft or invoice finance facility for the higher working capital requirement

Possibly a modest equity top-up from founders or investors to provide a safety buffer

Example 2: Acquisition and integration

A company acquires a smaller competitor.

A blended approach could include:

· Term loan or acquisition finance for the purchase price

· Equity investment to strengthen the balance sheet

Short-term facility to cover integration costs, with a clear plan for repayment within 12 to 18 months

Example 3: Early-stage growth

A fast-growing technology business with little tangible asset base might use:

· Seed or Series A equity funding as the core

· A small working capital line (overdraft or revenue-based facility) to smooth timing differences

Potentially asset finance for any hardware or equipment

The art is in building a funding stack that works together without overloading the business.

Pros, cons and common pitfalls

Key factors to consider

1. Cost

Not just the headline rate, but the total cost over time, including fees and charges.

2. Control

Equity investors may want a say in major decisions. Lenders may impose covenants and reporting requirements.

3. Security and guarantees

Many lenders will ask for personal guarantees or charges over assets. Founders should understand the real personal risk they are taking on.

4. Speed

Faster is often more expensive. There is a trade-off between quick decisions and cost.

5. Complexity and admin

Some facilities require regular reporting, reconciliations and covenant testing. This can be manageable with proper systems, but painful without them.

Common mistakes founders make

1. Leaving it too late

Approaching funders when cash is already critical reduces your options and bargaining power. The terms will usually be worse.

2. Chasing the fastest money, not the right money

As in Sarah’s story, choosing a product for speed rather than suitability can lead to a long, expensive hangover.

3. Ignoring the impact on personal risk

Signing personal guarantees without understanding the consequences if things go wrong.

4. Over-optimistic forecasts

Building funding plans on best-case scenarios, rather than realistic and downside cases.

5. Poor communication with lenders and investors

Surprising funders with bad news rarely goes well. Regular, honest communication builds trust and flexibility.

6. Not aligning funding with strategy

Funding decisions should support your long-term goals. There is no point in raising money in a way that makes a future sale or exit much harder.

A fractional CFO can help you avoid these traps by bringing an experienced, objective view and challenging assumptions before you commit.

The Upside of Getting Funding Right

When the funding structure fits the business, several good things happen.

Stability and resilience

You have enough headroom to absorb bumps in the road: a delayed payment, a lost customer, or a project that overruns. This reduces the constant firefighting and “cash panic” that drains energy from founders.

Capacity for growth

The right blend of equity and debt gives you the capacity to:

Take on bigger contracts

Invest in better systems and people

Enter new markets with confidence

Growth becomes intentional rather than accidental.

Better valuation and investor appeal

Well-structured funding, backed by clean financial information and clear reporting, makes your business more attractive to buyers and investors. They can see how growth is funded and where the returns will come from.

Founder peace of mind

Perhaps most importantly, you regain control. You know:

What you have borrowed

What it costs

How it will be repaid

How much risk you are personally carrying

That clarity reduces anxiety and lets you focus on running and growing the business.

Why work with a fractional CFO like Experius Consulting

Most founders did not go into business to spend their evenings building funding models and negotiating with lenders. Yet the funding decisions you make now will shape your business and your personal finances for years.

This is where an experienced fractional CFO partner adds real value.

At Experius Consulting, we:

Translate your strategy into numbers, so you can see how much funding you really need and when

Build simple, robust cash flow forecasts that lenders and investors can trust

Map your funding needs to the right mix of equity, debt and working capital facilities

Stress-test different options so you can see the impact on cash, profit and personal risk

Help you prepare information packs, board papers and lender presentations

Sit alongside you in discussions with banks, investors and alternative lenders, as your independent expert

We are not tied to any particular funder or product. Our role is to sit on your side of the table, helping you choose what is right for your business, not what is easiest to sell.

A clear next step

If you are:

Feeling under pressure from cash flow

Considering a major investment, acquisition or growth push

Already using short-term, high-cost funding and worried it is getting out of hand

Or simply unsure whether your current funding mix is fit for the future

then now is the time to have a structured conversation.

Experius Consulting can provide part-time, senior finance expertise, tailored to SMEs, at a fraction of the cost of a full-time CFO. Together, we can:

Clarify your funding needs

Design a sustainable funding strategy

Support you through applications, negotiations and implementation

So, you can get back to doing what you do best: building a business worth owning.